Good to Know: Choosing the Right Social Security Retirement Age

In an AARP survey taken of individuals aged 44 through 75, more than three of every five surveyed would choose death over running out of money in retirement. Helping a client maximize their Social Security Retirement benefit can begin addressing this deep-seated fear.

Coaching Opportunity

What if you, the Financial Adviser, could make your clients aware of how to:

- Get more, potentially much more, from their Social Security Retirement benefits,

- Relieve current income pressure on their retirement portfolio and

- Allow the portfolio to grow longer and larger?

A tuned-in Financial Advisor can do all of that by helping clients make informed decisions when claiming their Social Security Retirement benefit.

Key Point

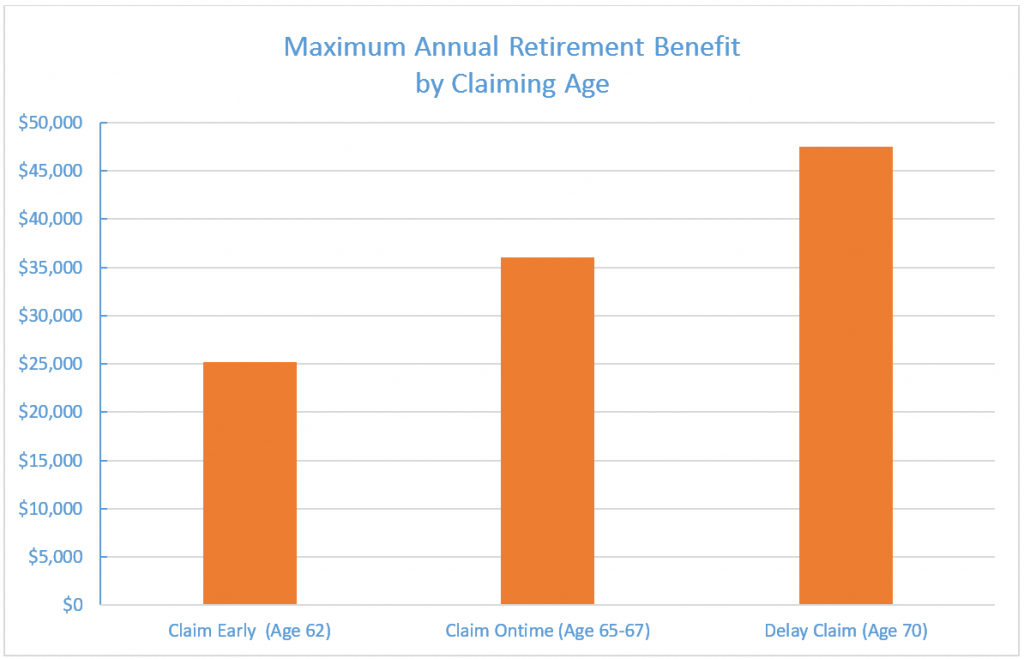

The challenge here is helping your client choose the right Social Security Retirement benefit claiming age for their individual situation. The claiming age is the age at which an individual claims Social Security Retirement benefits. In fact, it may be possible to increase a client’s Social Security Retirement benefit by as much as $20,000 or more annually for life just by choosing the right claiming age. The following chart illustrates just how impactful this decision can be.

Your client can claim benefits early, on time or on a delayed basis.

Based on claiming age and other factors, your client can receive an annual Social Security Retirement benefit in 2020 of as much $47,500 or as little as $25,200.

How about a 90% raise?

- Waiting until age 70 to claim can increase a client’s annual retirement benefit by almost 90% compared to claiming at age 62.

- The data in this chart assumes a client with above average earnings over his or her working lifetime.

- Clients with below average earnings will see a dramatic increase in benefits by delaying the claiming age to 70, but the dollar increase may be less than $20,000 annually.

Each claiming age choice has pitfalls and opportunities as summarized below.

Claim Early - Maximum Monthly Benefit $2,100 (2020)

- Background – Claiming early means the retiree gets a smaller benefit over a longer time period. The earliest your client can claim Social Security Retirement benefits is generally age 62. At that age, benefits are permanently reduced by as much as 30% based upon the claimant’s birth year. For example, a client born in or after 1960 receives only 70% of their full normal benefit (Primary Insurance Amount) if retirement benefits are claimed at age 62.

- Pitfall – Clients expected to live beyond the average life expectancy will generally receive significantly less in lifetime income by claiming at age 62 rather than waiting to claim at a later age. Average life expectancy for a 65-year-old is from age 82 (male) to age 85 (female). Yet, a healthy 65-year-old client with no major illness and within a recommended weight range can expect to live another 8 to 9 years - until about age 91 (male) to 93 (female).

- Opportunity – A client in poor health with a shortened life expectancy should consider claiming early. He or she may not live long enough to reap the benefits of waiting until normal retirement age or beyond to claim retirement benefits.

- Concern - Despite the severe financial downside of claiming early, almost 8 of every 10 eligible individuals claim retirement benefits early according to the AARP. In effect, these clients voluntarily chose a lifetime of drastically reduced benefits by collecting benefits too early!

Claim On Time - Maximum Monthly Benefit $3,011 (2020)

- Background – Claiming “on time” means the client will receive 100% of his or her full retirement benefit (Primary Insurance Amount) until death. Normal retirement age is 65 through 67 depending upon year of birth. A client in good health should consider waiting until at least normal retirement age to claim retirement benefits.

- Pitfall – Healthy clients who expect to live well beyond the average life expectancy would receive significantly less in lifetime income if they claim at normal retirement age instead of waiting until age 70 to claim.

- Opportunity – Waiting until at least normal retirement age to claim retirement benefits would provide more lifetime income than claiming at age 62, unless the client expects a relatively short life expectancy.

- Concern - Only about 1 in every 10 individuals waits until their normal retirement age to claim retirement benefits.

Delayed Claim - Maximum Monthly Benefit $4,000

- Background – Delayed claiming means your client will receive a larger check over a shorter period of time. Most clients will receive an 8% increase to their Social Security Retirement benefit for each year they delay claiming from normal retirement age through age 70.

- Pitfall – Delayed claiming is a bet that your client will outlive the average life expectancy. While a delayed claim should be considered for a client in good health, there are no guarantees when it comes to life expectancy. Analysts estimate it takes about 15 years to break even. For example, a client who claims at age 70 would generally have to live until about age 85 before the cumulative increased benefits from delayed claiming would offset the “lost income” from not claiming at normal retirement age.

- Opportunity – Retirement benefits increase by a total of as much as 32% when clients wait until age 70 to claim benefits. Key additional benefits to a delayed claim include:

- Higher benefit for surviving spouse - The client’s surviving spouse will receive 100% of the client’s increased benefit for life when the client dies.

- More time to grow the retirement portfolio - Waiting until age 70 may allow the client’s retirement portfolio to increase in value, assuming that income from the portfolio is not required until age 70.

- Concern – Far less than 1 of every 10 clients delay claiming until age 70.

Conclusion and Financial Advisor Opportunity

Coaching clients to better claiming age decisions can provide a much better client retirement lifestyle and provide opportunities to grow your own practice.

Financial Advisor Opportunity

The claiming age discussion can lead to a broader conversation around retirement income planning as a whole. Retirement income from Social Security, IRAs, and employer-sponsored retirement plans should be coordinated to generate the maximum retirement income at the lowest tax cost. Coordination can lead to consolidation of investments from other providers and annuity sales.

For more information, join us at Coaching and Engagement Blog Posts.

Remember to consult your compliance department, financial planning team, or CFP® Certificant before discussing these issues with clients.

The information presented herein is provided purely for educational purposes and to raise awareness of these issues; it is not meant to provide and should not be used to provide legal or financial advice to clients. There are variations, alternatives, and exceptions to this material that could not be covered within the scope of this blog.