Managing Concentration Wealth Risk — Swap (Exchange) Fund

Good to Know

Purpose

The goal of a swap fund is to reduce concentration of wealth risk through a unique approach to diversification. We will review this intriguing strategy's operation, legal structure, tax implications, pros, and cons.

Operation

A swap fund (after this referred to as “the fund”) is a pool of concentrated positions in different companies from different investors. In exchange for an investor’s concentrated position, the fund issues ownership interests in the fund’s portfolio to the investor, thereby providing the investor with diversification. However, the fund manager has the authority to reject or accept an investor’s shares. For example, a fund that holds all of the technology stock the fund manager deems prudent may not accept an additional technology stock.

The fund may operate for a fixed number of years or have no specific termination date, passing out earnings to the investors. When the fund is closed or terminated, participants do NOT generally receive back their contributed stocks. Instead, they receive back a portion of the diversified shares held in the fund. The end result is that investors eventually receive outright ownership in a diversified portfolio, with deferral of the capital gains tax.

Be careful not to confuse swap funds with exchange-traded funds (ETFs). Key differences are identified in the following chart.

| Swap Fund | ETF |

| Accepts contribution of concentrated positions | Accepts Cash Contributions |

| May be privately or publicly traded | Publicly traded only |

| Tax-free exchange for other securities | No tax-free exchanges |

Legal Structure

A swap fund is generally structured as a limited partnership in which numerous qualified investors (50-499) contribute their acceptable stock holding in return for a limited partnership interest in the fund. Even restricted stock contributions may be accepted in some cases. Once the fund is formed, it is closed to new investors and is passively managed. A general partner controls the partnership and may delegate investment responsibilities to a fund manager.

These funds may or may not trade in the secondary market, depending upon the pool of investments. Fund pools comprised only of publicly traded stock may trade in the secondary market while pools of private equity securities do not.

Non-Taxable Exchange

The beauty of a swap is tax deferral. Not only does the investor achieve diversification, but the exchange itself is tax-free. Only when the limited partnership interest obtained by the investor in the fund is sold at a gain will there be reportable capital gain. The exchange itself is income-tax-free, provided the fund holds at least 20 percent of the total capital in non-liquid assets, such as real estate. Equally important, the swap is NOT considered a constructive sale, which could cause recognition of gain at the swap date.

Caveats

- Federal requirements are for a holding period of 7 years to achieve non-recognition of gain or loss on the contribution.

- If an investor makes a withdrawal before that time, not only may there be early withdrawal penalties assessed by the fund, but the investor is likely to suffer recognition of capital gains.

- Only if an early withdrawal was for the return of the originally contributed asset could an investor avoid triggering the capital gain, but the choice of securities returned is at the discretion of the General Partner.

- Thus, investors should generally consider an exchange fund only when they can comfortably commit to leaving the contribution in the fund for the long term.

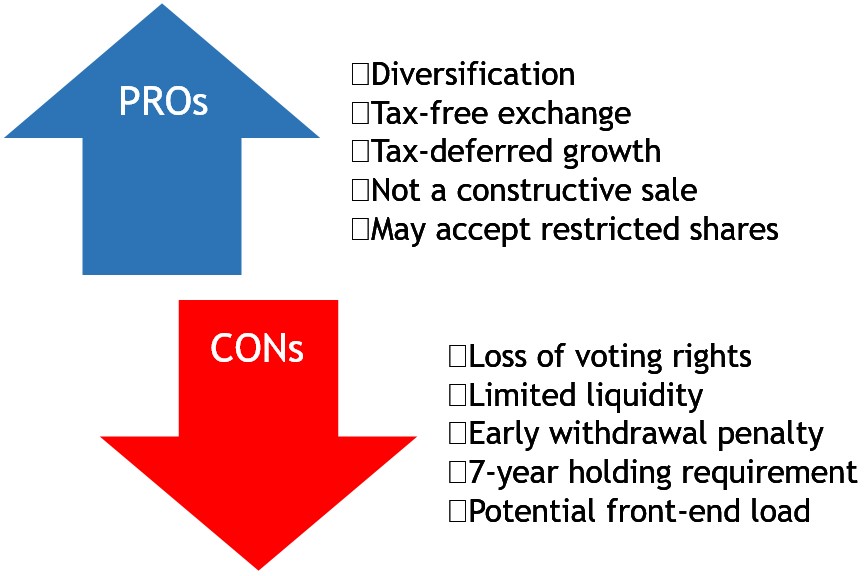

Pros and Cons

Summary

Concentrated wealth risk is real. Consider just one bank stock, for example. The bank was ranked in the top 5 nationally. The bank had a cadre of loyalists for whom selling or even hedging was heresy. Infamously, the stock price fell off of a cliff, plummeting from about $40/share to $1/share during a 10-month period. At one point, trading was halted in the stock.

Swap funds are one approach to diversifying out of a concentrated position. In our next blog, we’ll review how the prepaid variable forward strategy can also be used to manage concentration of wealth risk.