Protect Concentrated Positions With No Out-of-Pocket Cost

Good to Know

Unmanaged concentrated position risk can be a ticking time bomb in your client’s portfolio. For example, one of the nation’s oldest (founded in 1879) and most respected banks was trading at $38/share in 2007. It had a long-term, loyal stockholder following, many of whom with holdings — accumulated over generations — valued from $10 million to $100 million. Ten months later, the nation was shocked when the company collapsed. Share prices fell to $1/share before trading was halted.

Unmanaged concentrated position risk can be a ticking time bomb in your client’s portfolio. For example, one of the nation’s oldest (founded in 1879) and most respected banks was trading at $38/share in 2007. It had a long-term, loyal stockholder following, many of whom with holdings — accumulated over generations — valued from $10 million to $100 million. Ten months later, the nation was shocked when the company collapsed. Share prices fell to $1/share before trading was halted.

A shareholder with a $10 million position before the collapse who sold at $1/share saw their wealth plummet by over 97% to just $263 thousand. The bank was eventually sold to a competitor for $5.87/share. Shareholders were generally aware of this risk but thought nothing could take down their 128-year-old bank. Tragically, many of those very same shareholders needlessly lost their wealth due to unmanaged concentration risk.

This article continues our series on managing concentrated wealth risk by analyzing Zero Premium Collars. We’ll define this strategy, identify its pros and cons, illuminate potential tax issues, and provide an example.

Zero Premium Collar Defined

A collar is defined by Webster — in the context of a person’s apparel — as a “band, strip, or chain worn around the neck.” From one perspective, the collar to the right establishes a boundary, or limit, around the wearer’s neck. Similarly, investors build derivative collars to set limits around a stock’s price. A derivatives collar can be a powerful solution for the client concerned about downside risk in a concentrated position but with limited resources to buy put options.

A collar is defined by Webster — in the context of a person’s apparel — as a “band, strip, or chain worn around the neck.” From one perspective, the collar to the right establishes a boundary, or limit, around the wearer’s neck. Similarly, investors build derivative collars to set limits around a stock’s price. A derivatives collar can be a powerful solution for the client concerned about downside risk in a concentrated position but with limited resources to buy put options.

While holding a put option can protect against downside risk, which is the most significant risk to an equity concentration, the cost of the put option may be prohibitively expensive for some clients. To offset that expense, investors often generate the income needed to pay for the put by writing a call option. A “zero-premium collar” is structured so that the premium expense of the put equals the premium income from the call.

Pros and Cons

| Pro | Cons |

| The Put is the Floor

The put option establishes a floor below which your client avoids further losses. If the market price drops below the put exercise price, your client can exercise the put and sell at the put’s exercise price. |

The Call is the Ceiling

The call option establishes a ceiling above which your client will not participate in further gains. If the market price rises above the call’s exercise price, the call option owner will exercise the call and buy the shares from your client. |

| Retains appreciation potential up to call strike price | Potential requirement to collateralize the call with the shares owned |

| May customize option strike prices, maturities, and settlement features if created in the over-the-counter market | Potential income tax issues |

Tax Traps for the Unwary

Potential tax traps include the Constructive Sale Trap and the Straddle Trap.

Constructive Sale Trap

Suppose a collar “eliminates effectively all” the risk of holding a stock. The IRS would treat the collar as a constructive sale, and your client would have to report capital gains immediately. But what does it mean to “effectively eliminate” the risk? Your friends at the IRS specify that a collar structured within an IRS-acceptable range around the current price will avoid the constructive sale rule. The range described in the example below would generally be an acceptable range. The client should consult his or her tax advisor for additional information.

Straddle Trap

Any time your client has two separate and offsetting positions, as with a collar, it is termed a “straddle” and subject to the IRS straddle rules. These rules can limit deductible losses and accelerate the recognition of gains. The solution is a one-contract collar in which both the puts and calls are contained within one options contract. These one-contract collars can be created either with put and call options or variable prepaid forwards. If options are used, they must be privately negotiated in the over-the-counter market in order to place them in a single contract.

Example

Some would say that collar strategies can be structured in ways limited only by your imagination. That may be a bit of an overstatement, but collar strategies can be incredibly flexible and complex. We’ll provide an example of a simple protective collar strategy. First, let’s dispense with two terms — protective collar and long option.

- The primary purpose of a protective collar is to protect the investor from sharp drops in the share price.

- A long option is an option on shares the investor owns.

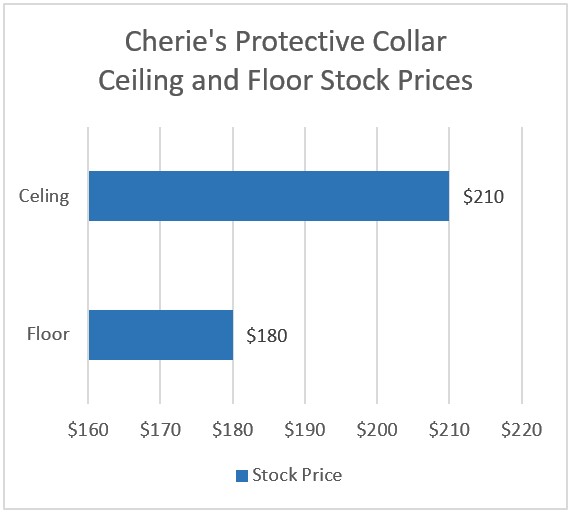

Now, to the example. Your client Cherie owns 10,000 shares of Genesis, Inc., trading at $200 per share. She is primarily concerned about downside risk, lacks the resources to buy puts, and ideally, she’d like to keep the stock. After considering a collar strategy:

- She sold 10,000 one-year, long calls at $10/share with a strike price of $210 and

- At the same time, she paid $10/share to acquire 10,000 one-year, long put options with a strike price of $180.

The net result? Cherie gained protection from downside risk at the opportunity cost of upside potential. Here’s a graph illustrating her collar.

Downside risk protected— If the share price drops below the $180/share floor, she will exercise her put option and sell at $180/share.

Downside risk protected— If the share price drops below the $180/share floor, she will exercise her put option and sell at $180/share.

Upside potential lost — If the share price appreciates above $210/share, the call option owner will exercise and buy her shares at $210.

If the share price remains between $180 and $210, neither the put nor the call option is likely to be exercised. Cherie would have protected her downside risk at zero premium cost and would still own the stock.

Summary

The key here is finding a zero-premium strategy that balances a client’s need for downside protection against an acceptable limit on the upside potential. While the goal is zero premium cost, the reality is that a small premium cost may be required to gain more downside protection or upside participation for the client’s needs. Managing concentrated wealth is seldom a one-size-fits-all solution. Financial advisors with clients holding concentrated positions need to understand these strategies to keep clients and potentially grow revenues. Click here to gain that understanding.