Wake Up Call for Retirement Savings

Good to Know

Let’s frame the challenge faced by far too many Americans. Confidence in a comfortable retirement remains soberingly low. Consider this:

- Less than half of Americans feel confident about their retirement savings,

- Nearly one-third of Americans plan to depend solely on Social Security for retirement income, and

- The average annual Social Security benefit is projected to be about $24,000 in 2025 (that’s only about $9,000 above the federal poverty level).

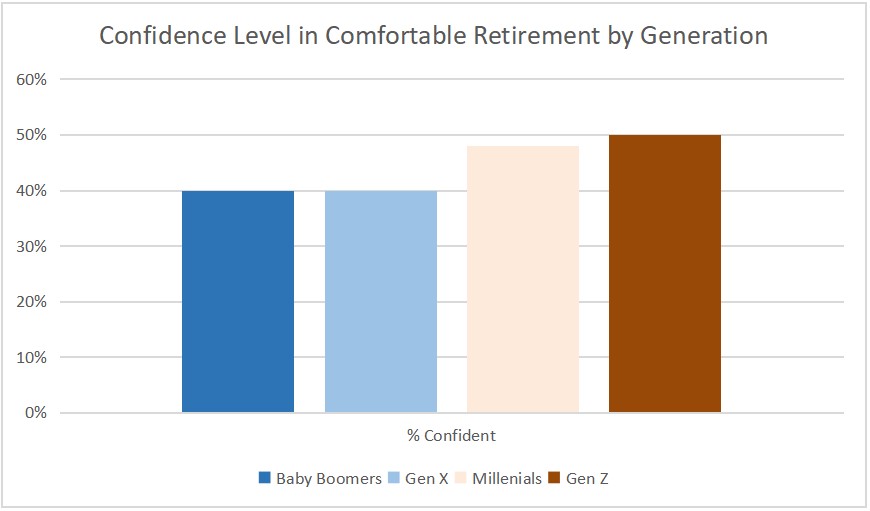

We see slight differences in retirement confidence by generation, as illustrated by the chart that follows.

Retirement Confidence by Generation

Key point — no generation expressed more than a 50% confidence level in their retirement income. Intuitively, retirement savings by age differed dramatically by generation.

Key point — no generation expressed more than a 50% confidence level in their retirement income. Intuitively, retirement savings by age differed dramatically by generation.

Retirement Savings by Age

Median retirement savings by age may at least partially explain the dearth of retirement confidence.

- Under 35:The median retirement account balance is approximately $18,880.

- Ages 35-44:Median savings increase to around $45,000.

- Ages 45-54:Median retirement savings reach about $115,000.

- Ages 55-64:Median balances are approximately $185,000.

- Ages 65-74:Median savings peak at around $200,000

We can interpret these numbers in one of two ways:

- Do nothing because it’s a challenge, or

- Confront the challenge — act now to improve your retirement lifestyle.

How to Improve Retirement Readiness

For baby boomers — contact your financial advisor now to discuss ways to increase your retirement income by:

- Health permitting, consider delayed claiming for Social Security Retirement benefits past your normal retirement age (65 to 67 depending on birth year) to capture delayed retirement credits of 8% per year,

- Ensure that your portfolio reflects your risk tolerance,

- Downsize your home and add the potentially tax-free gains to your portfolio,

- Work part-time in retirement doing something you enjoy doing, or

- Other alternatives your financial advisor may suggest.

For Millennials, Gen Z, and Gen X — consult your financial advisor now to:

- Start saving — time and the power of compounding are your friends,

- Save more —save a higher percentage of income, especially during peak earning years,

- Max the match — if your employer offers a 401(k) plan, defer as much as you can, even if that means cutting discretionary spending, but at least defer enough to get the maximum employer matching contribution (if available), and

- Diversify Investments — Taking on too much risk can wreck a retirement plan with large losses as you near retirement while taking on too little risk will likely reduce returns — maintain a balanced portfolio based on your own risk tolerance (your financial advisor can help you here) to optimize risk-adjusted returns.

In closing, there is wisdom in the immortal words of Ben Feldman.

Doing something costs something. Doing nothing costs something. And, quite often, doing nothing costs a lot more!

If you’re interested in becoming a CFP® Professional, we welcome the opportunity to support you in that journey. Visit https://www.financialplannerprogram.com/ or speak to one of our enrollment advisors at 404.324.4600, x111 to learn more about our partner CFP® Certification Education programs.

Financial advisors and planners need a sound understanding of the competitive edge of joining the ranks of highly-trusted financial professionals. Get that sound understanding through our CFP® Curriculum when you consider CFP® certification. You’ll discover a select few of the reasons our student pass rates are much higher than the national averages.

The material contained in this article is to raise awareness—it is informational, general in nature and does not constitute financial advice. It should not be relied upon or used without consulting a credentialed financial professional to consider your specific circumstances. This communication was published on the date specified and may not include any future changes in the topics, laws, rules or regulations covered.